● Live

MACD Liquidity Spectrum by @DaviddTech 🤖 [ee9cffed]

🛡️ MACDLIQUIDITYSPECTRUM WIFUSDT 5M 7.05

Trading Pair

WIF

Base Currency

Performance Overview

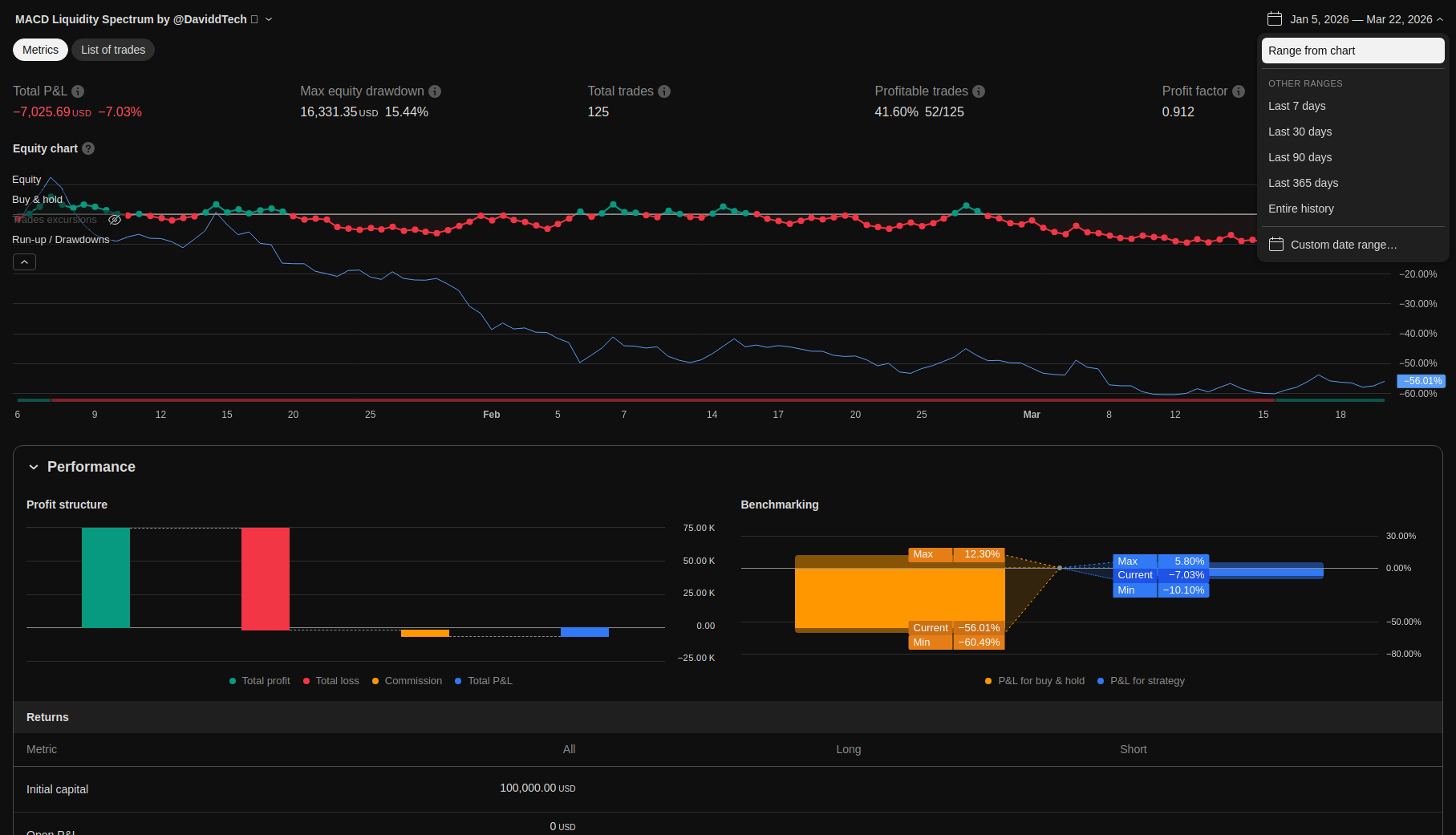

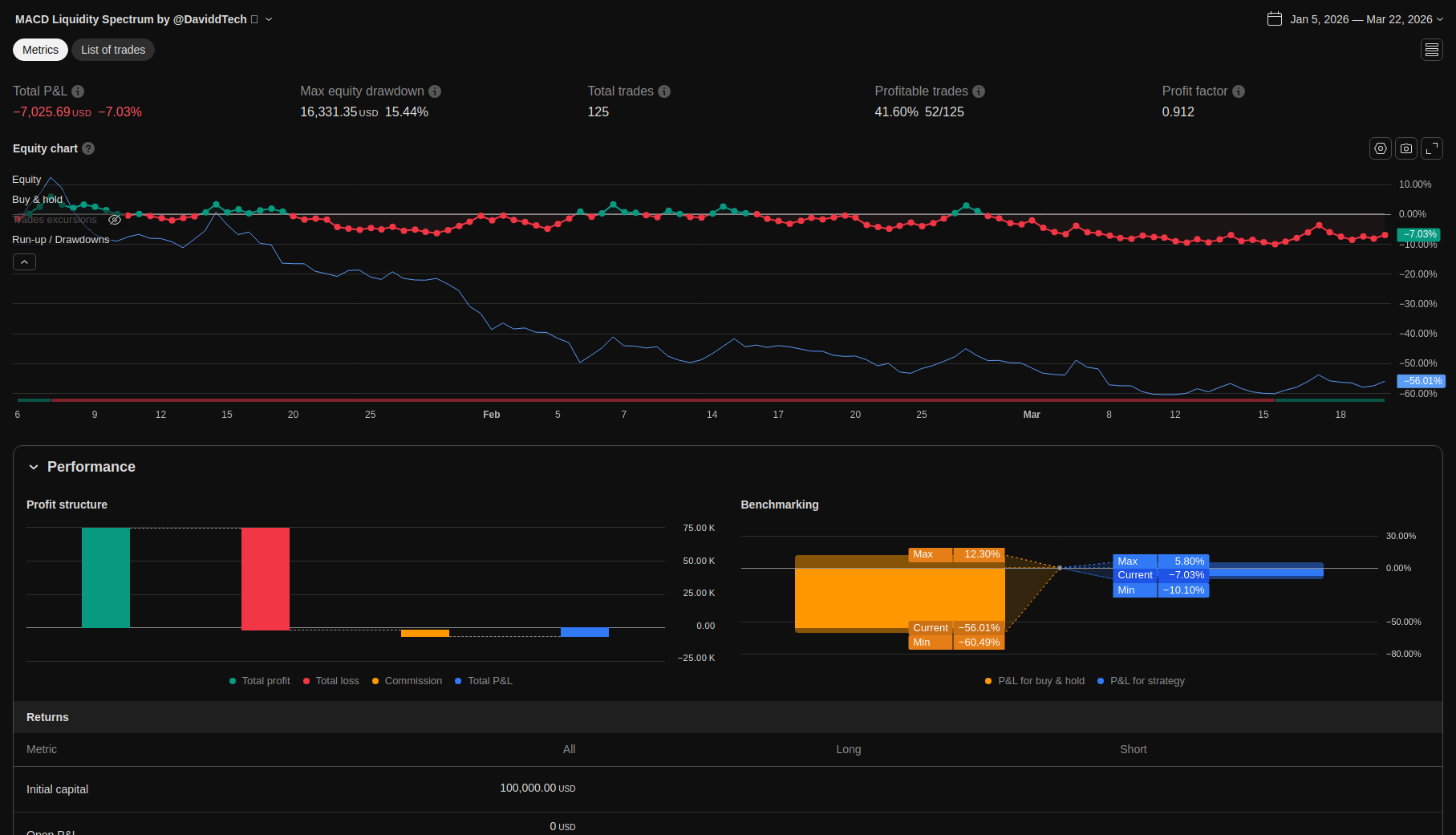

Total Return

Primary

-7.03%

Net Profit Performance

Win Rate

Success

41.6%

Trade Success Ratio

Max Drawdown

Risk

%

Risk Control

Profit Factor

Efficiency

0.912

Risk-Reward Ratio

Incubation Delta

Live

-2.02%

Live vs Backtest

Total Trades

Volume

125

Executed Trades

Equity Curve Analysis

Performance comparison between backtest and live trading results

Backtest Performance

Live Trading

First Trade

Jan 6, 2026

169

Days

125

Trades

Last Trade

Mar 22, 2026

All backtests include realistic trading fees and slippage

Strategy Analysis & Data

Comprehensive performance metrics and detailed analysis

Performance Metrics

Detailed trading performance analysis and key metrics

Trades per Day

Key Performance Metrics

- First Traded Date: 2026-01-06 15:30:00

- Sharpe Ratio: -0.05

- Sortino Ratio: -0.07

- Calmar: 2.00

- Longest DD Days: 121.00

- Volatility: 22.66

- Skew: 0.27

- Kurtosis: -0.79

- Expected Daily: -0.04

- Expected Monthly: -0.75

- Expected Yearly: -8.59

- Kelly Criterion: -5.14

- Daily Value-at-Risk: -2.44

- Expected Shortfall (cVaR): -2.53

- Last Trade Date: 2026-03-22 00:35:00

- Max Consecutive Wins: 4

- Number Winning Trades 52

- Max Consecutive Losses: 6

- Number Losing Trades: 73

- Gain/Pain Ratio: 2.00

- Gain/Pain (1M): 0.89

- Payoff Ratio: 1.29

- Common Sense Ratio: 0.89

- Tail Ratio: 1.01

- Outlier Win Ratio: 2.12

- Outlier Loss Ratio: 0.00

- Recovery Factor: 0.00

- Ulcer Index: 0.09

- Serenity Index: -0.73

Trade Analysis

Individual trade breakdown and analysis

List of Trades

Key : Pink Background = Live Trades | Black Background = Backtest Trades

Monthly Profit & Loss

Monthly performance breakdown with profit/loss indicators

📊 Detailed Monthly Performance Analysis

Comprehensive monthly breakdown showing both cumulative (compounded) returns and simple P&L sums. Each cell displays both metrics for complete transparency.

Incubation Period

Live Trading

| Year/Month | January | February | March | April | May | June | July | August | September | October | November | December |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026 | Login to see results | Login to see results | Login to see results | Login to see results | Login to see results | Login to see results | +0.00% +0.00% Simple P&L | +0.00% +0.00% Simple P&L | +0.00% +0.00% Simple P&L | +0.00% +0.00% Simple P&L | +0.00% +0.00% Simple P&L | +0.00% +0.00% Simple P&L |

Live Trading Statistics

Real-time trading performance and statistics

Live Trades Stats

125

Number of Trades

-2.02%

Cumulative Returns

41.6%

Win Rate

2024-05-07

🟠 Incubation started

🛡️

7 Days

0%

30 Days

0%

60 Days

0%

90 Days

Strategy Audit & Screenshots

Visual verification of strategy performance with TradingView screenshots

| All USD | All % | Long USD | Long % | Short USD | Short % | |

|---|---|---|---|---|---|---|

| Initial Capital | 100000 | |||||

| Open P&l | 0 | 0.0 | ||||

| Net Profit | -7025.69 | -7.03 | -13181.3 | -13.18 | 6155.62 | 6.16 |

| Gross Profit | 72572.75 | 72.57 | 45084.43 | 45.08 | 27488.33 | 27.49 |

| Gross Loss | 79598.44 | 79.6 | 58265.73 | 58.27 | 21332.71 | 21.33 |

| Expected Payoff | -56.21 | -188.3 | 111.92 | |||

| Commission Paid | 4854.75 | 2722.71 | 2132.04 | |||

| Buy & Hold Return | -58261.81 | -58.26 | ||||

| Buy & Hold % Gain | -58.26 | |||||

| Strategy Outperformance | 51236.13 | |||||

| Max Contracts Held | 285080 | 275027.0 | 285080.0 | |||

| Annualized Return (cagr) | -29.39 | -49.09 | 33.02 | |||

| Return On Initial Capital | -7.03 | -13.18 | 6.16 | |||

| Account Size Required | 16331.35 | |||||

| Return On Account Size Required | -43.02 | -80.71 | 37.69 | |||

| Avg Margin Used | 0 | |||||

| Max Margin Used | 0 | |||||

| Margin Efficiency | 0 | 0.0 | 0.0 | |||

| Avg Equity Run-up Duration (close-to-close) | 3 days | |||||

| Avg Equity Run-up (close-to-close) | 5233.17 | 5.23 | ||||

| Max Equity Run-up (close-to-close) | 7391.32 | 7.39 | ||||

| Max Equity Run-up (intrabar) | 10593.55 | 9.72 | ||||

| Max Equity Run-up As % Of Initial Capital (intrabar) | 10.59 | |||||

| Avg Equity Drawdown Duration (close-to-close) | 68 days | |||||

| Avg Equity Drawdown (close-to-close) | 15903.47 | 15.9 | ||||

| Return Of Max Equity Drawdown | -0.43 | -0.81 | 0.38 | |||

| Max Equity Drawdown (close-to-close) | 15903.47 | 15.9 | ||||

| Max Equity Drawdown (intrabar) | 16331.35 | 15.44 | ||||

| Max Equity Drawdown As % Of Initial Capital (intrabar) | 16.33 | |||||

| Net Profit As % Of Largest Loss | -260.94 | -489.57 | 357.55 | |||

| Largest Winner As % Of Gross Profit | 4.52 | 7.28 | 8.39 | |||

| Largest Loser As % Of Gross Loss | 3.38 | 4.62 | 8.07 | |||

| Total Open Trades | 0.0 | 0.0 | 0.0 | |||

| Total Closed Trades | 125.0 | 70.0 | 55.0 | |||

| Number Winning Trades | 52.0 | 27.0 | 25.0 | |||

| Number Losing Trades | 73.0 | 43.0 | 30.0 | |||

| Even Trades | 0.0 | 0.0 | 0.0 | |||

| Percent Profitable | 41.6 | 38.57 | 45.45 | |||

| Avg P&l | -56.21 | -0.09 | -188.3 | -0.36 | 111.92 | 0.25 |

| Avg Winning Trade | 1395.63 | 2.88 | 1669.79 | 3.44 | 1099.53 | 2.28 |

| Avg Losing Trade | 1090.39 | 2.21 | 1355.02 | 2.74 | 711.09 | 1.45 |

| Ratio Avg Win / Avg Loss | 1.28 | 1.232 | 1.546 | |||

| Largest Winning Trade | 3280.79 | 3280.79 | 2307.5 | |||

| Largest Winning Trade Percent | 6.42 | 6.42 | 4.72 | |||

| Largest Losing Trade | 2692.45 | 2692.45 | 1721.6 | |||

| Largest Losing Trade Percent | 5.08 | 5.08 | 3.44 | |||

| Avg # Bars In Trades | 84.0 | 96.0 | 69.0 | |||

| Avg # Bars In Winning Trades | 86.0 | 80.0 | 92.0 | |||

| Avg # Bars In Losing Trades | 83.0 | 106.0 | 50.0 | |||

| Sharpe Ratio | -0.048 | |||||

| Sortino Ratio | -0.072 | |||||

| Profit Factor | 0.912 | 0.774 | 1.289 | |||

| Margin Calls | 0.0 | 0.0 | 0.0 |

| All USD | All % | Long USD | Long % | Short USD | Short % | |

|---|---|---|---|---|---|---|

| Initial Capital | 100000 | |||||

| Open P&l | 0 | 0.0 | ||||

| Net Profit | -7025.69 | -7.03 | -13181.3 | -13.18 | 6155.62 | 6.16 |

| Gross Profit | 72572.75 | 72.57 | 45084.43 | 45.08 | 27488.33 | 27.49 |

| Gross Loss | 79598.44 | 79.6 | 58265.73 | 58.27 | 21332.71 | 21.33 |

| Expected Payoff | -56.21 | -188.3 | 111.92 | |||

| Commission Paid | 4854.75 | 2722.71 | 2132.04 | |||

| Buy & Hold Return | -58261.81 | -58.26 | ||||

| Buy & Hold % Gain | -58.26 | |||||

| Strategy Outperformance | 51236.13 | |||||

| Max Contracts Held | 285080 | 275027.0 | 285080.0 | |||

| Annualized Return (cagr) | -29.39 | -49.09 | 33.02 | |||

| Return On Initial Capital | -7.03 | -13.18 | 6.16 | |||

| Account Size Required | 16331.35 | |||||

| Return On Account Size Required | -43.02 | -80.71 | 37.69 | |||

| Avg Margin Used | 0 | |||||

| Max Margin Used | 0 | |||||

| Margin Efficiency | 0 | 0.0 | 0.0 | |||

| Avg Equity Run-up Duration (close-to-close) | 3 days | |||||

| Avg Equity Run-up (close-to-close) | 5233.17 | 5.23 | ||||

| Max Equity Run-up (close-to-close) | 7391.32 | 7.39 | ||||

| Max Equity Run-up (intrabar) | 10593.55 | 9.72 | ||||

| Max Equity Run-up As % Of Initial Capital (intrabar) | 10.59 | |||||

| Avg Equity Drawdown Duration (close-to-close) | 68 days | |||||

| Avg Equity Drawdown (close-to-close) | 15903.47 | 15.9 | ||||

| Return Of Max Equity Drawdown | -0.43 | -0.81 | 0.38 | |||

| Max Equity Drawdown (close-to-close) | 15903.47 | 15.9 | ||||

| Max Equity Drawdown (intrabar) | 16331.35 | 15.44 | ||||

| Max Equity Drawdown As % Of Initial Capital (intrabar) | 16.33 | |||||

| Net Profit As % Of Largest Loss | -260.94 | -489.57 | 357.55 | |||

| Largest Winner As % Of Gross Profit | 4.52 | 7.28 | 8.39 | |||

| Largest Loser As % Of Gross Loss | 3.38 | 4.62 | 8.07 | |||

| Total Open Trades | 0.0 | 0.0 | 0.0 | |||

| Total Closed Trades | 125.0 | 70.0 | 55.0 | |||

| Number Winning Trades | 52.0 | 27.0 | 25.0 | |||

| Number Losing Trades | 73.0 | 43.0 | 30.0 | |||

| Even Trades | 0.0 | 0.0 | 0.0 | |||

| Percent Profitable | 41.6 | 38.57 | 45.45 | |||

| Avg P&l | -56.21 | -0.09 | -188.3 | -0.36 | 111.92 | 0.25 |

| Avg Winning Trade | 1395.63 | 2.88 | 1669.79 | 3.44 | 1099.53 | 2.28 |

| Avg Losing Trade | 1090.39 | 2.21 | 1355.02 | 2.74 | 711.09 | 1.45 |

| Ratio Avg Win / Avg Loss | 1.28 | 1.232 | 1.546 | |||

| Largest Winning Trade | 3280.79 | 3280.79 | 2307.5 | |||

| Largest Winning Trade Percent | 6.42 | 6.42 | 4.72 | |||

| Largest Losing Trade | 2692.45 | 2692.45 | 1721.6 | |||

| Largest Losing Trade Percent | 5.08 | 5.08 | 3.44 | |||

| Avg # Bars In Trades | 84.0 | 96.0 | 69.0 | |||

| Avg # Bars In Winning Trades | 86.0 | 80.0 | 92.0 | |||

| Avg # Bars In Losing Trades | 83.0 | 106.0 | 50.0 | |||

| Sharpe Ratio | -0.048 | |||||

| Sortino Ratio | -0.072 | |||||

| Profit Factor | 0.912 | 0.774 | 1.289 | |||

| Margin Calls | 0.0 | 0.0 | 0.0 |

TradingView Screenshots

Slide this way to reveal live trades

USE SLIDER TO REVEAL RESULTS

Slide this way to reveal backtest

Slide this way to reveal live trades

USE SLIDER TO REVEAL RESULTS

Slide this way to reveal backtest

⚪️ Other Backtest

AI Quantitative Analysis

Advanced AI-powered insights and strategy analysis

AI Quantitative Analyst

Ready to analyze

Risk Analysis

Performance Metrics

Market Insights

📈 Risk-Reward Analysis

📊 Performance Metrics

🎯 Market Comparison

Advanced Markov Motor Analysis

Sophisticated analysis of strategy edge degradation, rolling metrics, and Markov chain properties

Analysis Controls

Live Analysis

20

trades

1.2

PF

Rolling Performance Metrics

Current Trend

Analyzing...

Edge Strength

Calculating...

Markov State Transitions

W

L

Win/Loss States

Transition Probabilities

From/To

Win

Loss

Win

0.00

0.00

Loss

0.00

0.00

Edge Decay Analysis

Edge Intact

Consistency Score

--

Stability Index

--

Trend Strength

--

Return Distribution Analysis

Skewness

--

Kurtosis

--

Tail Risk

--

Market Regime Detection

Analyzing...

Favorable Regime %

--

Avg Regime Duration

--

Current Regime Age

--

Markov Intelligence Insights

Analyzing strategy patterns...

Choose your Reaction!